How the Federal Reserve’s Next Move Could Impact the Housing Market

September 4, 2024

September 4, 2024

As we enter September, all eyes are on the Federal Reserve (the Fed) and its next move, which could have significant implications for the housing market. Speculation is high that the Fed will cut the Federal Funds Rate in its upcoming meeting. This comes on the heels of improving inflation data and signs of a slowdown in the job market. According to Mark Zandi, Chief Economist at Moody’s Analytics, the Fed is likely to move forward with a rate cut unless inflation surprises them, which he believes is unlikely.

But what does a potential rate cut mean for homebuyers and sellers? Let’s break it down.

Why a Federal Funds Rate Cut Matters

The Federal Funds Rate directly influences mortgage rates. Though it’s not the only factor (geopolitical events, the economy, and market demand all play roles), a cut in the Federal Funds Rate often signals lower mortgage rates on the horizon.

Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), notes that once the Fed begins cutting rates, mortgage rates tend to follow, albeit gradually. The initial cut likely won’t cause mortgage rates to plummet, but it can contribute to a steady decline over time.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), predicts that this won’t be a one-and-done move. “Six to eight rounds of rate cuts all through 2025 look likely,” Yun says.

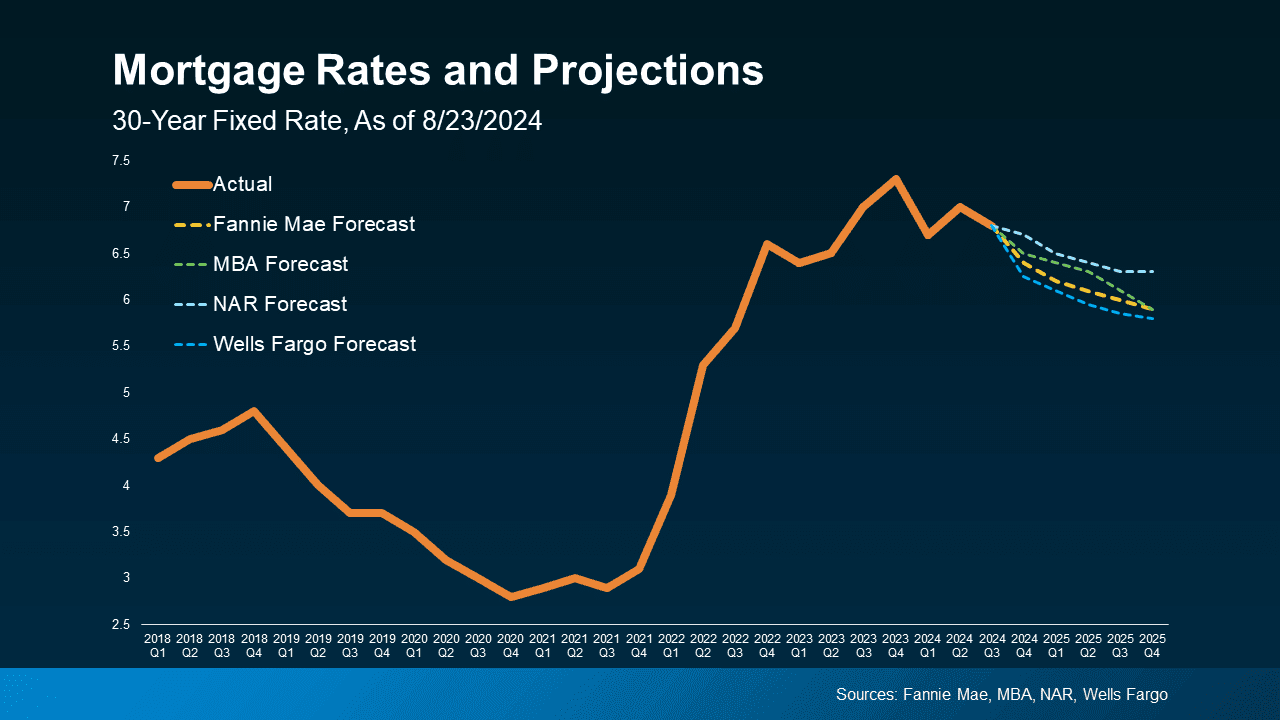

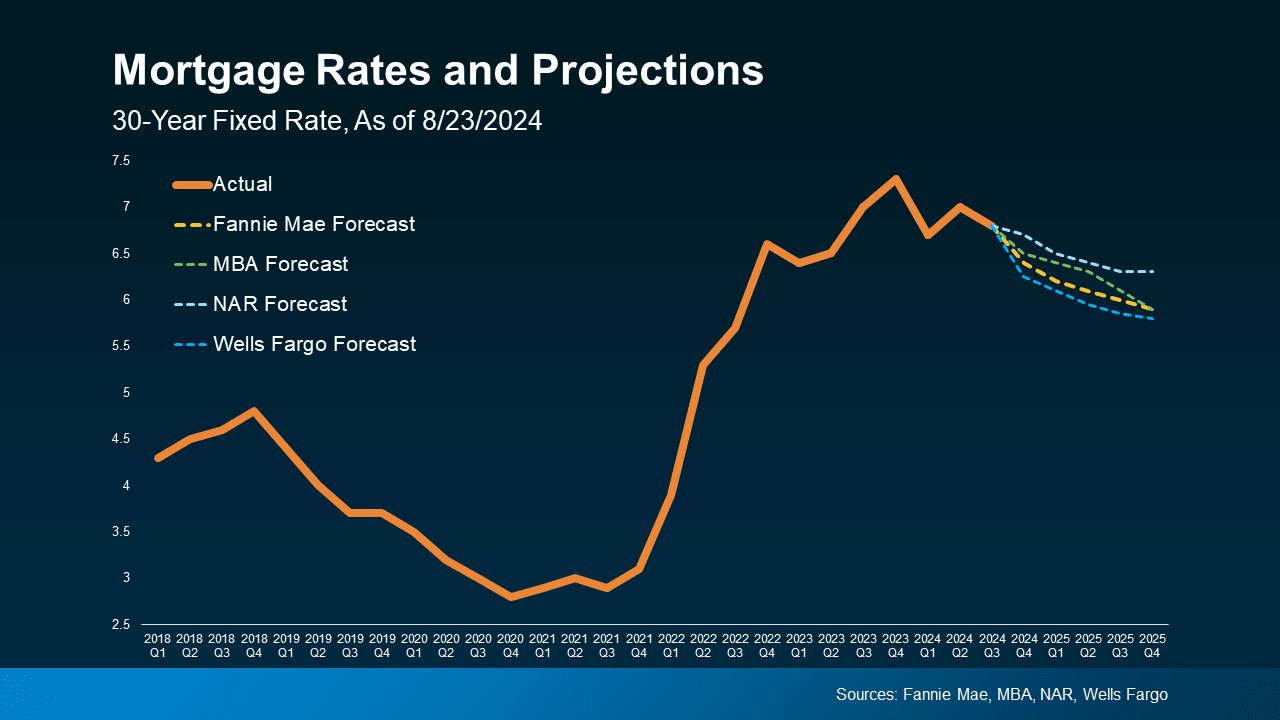

Projected Mortgage Rate Trends

With the Fed likely to kick off a series of rate cuts, experts project that mortgage rates will decrease gradually over the next two years. As seen in the graph below, which includes forecasts from Fannie Mae, the Mortgage Bankers Association, NAR, and Wells Fargo, all point to a moderate decline in mortgage rates through 2025.

This is good news for both homebuyers and sellers, but how exactly will it impact the market?

The Benefits for Buyers and Sellers

1. Easing the Lock-In Effect

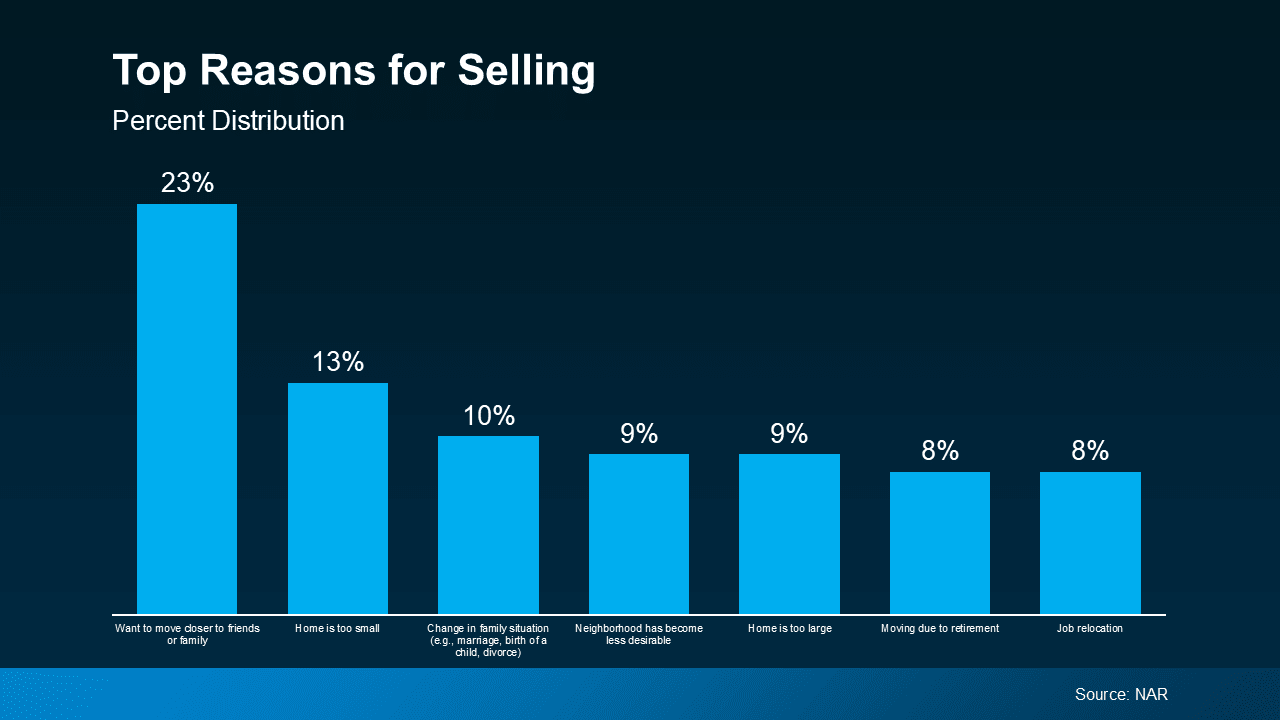

Many current homeowners have been hesitant to sell their homes due to the “lock-in effect.” They secured low mortgage rates when they purchased their homes, and with today’s higher rates, many are reluctant to sell and take on a more expensive mortgage.

A gradual decline in rates could ease this effect, making it more attractive for homeowners to sell. However, it’s not expected to trigger a massive surge in new listings, as many homeowners will still be cautious about giving up their existing rates.

2. Boosting Buyer Activity

For buyers, a decline in mortgage rates will reduce the overall cost of purchasing a home. As rates gradually decrease, more buyers who were previously priced out of the market may find homeownership within reach. This increased buyer activity could lead to a healthier, more balanced housing market.

What Should Buyers and Sellers Do Now?

While the Fed’s anticipated rate cut will likely contribute to a gradual decrease in mortgage rates, it’s important not to wait for the perfect time to buy or sell. As Jacob Channel, Senior Economist at LendingTree, says, “Timing the market is basically impossible. If you’re always waiting for perfect market conditions, you’re going to be waiting forever.”

If buying or selling a home makes sense for you now, take action. The Fed’s upcoming moves could work in your favor, but don’t let market timing hold you back.

Bottom Line

The Federal Reserve’s expected rate cuts, driven by improved inflation data and slower job growth, are likely to lead to a gradual decline in mortgage rates through 2025. While this presents new opportunities for buyers and sellers, it’s important to make decisions based on your personal circumstances rather than waiting for the “perfect” market conditions.

If you’re ready to take the next step in your real estate journey, let’s connect today to discuss how the evolving market can impact your homeownership goals.

Stay up to date on the latest real estate trends.

January 14, 2026

How to Price Your Home For A Faster Sale

September 10, 2024

Navigating the Shifting Housing Market: No Crash in Sight

September 4, 2024

Understanding Why Homeowners Are Selling and How Rate Cuts May Boost the Market

September 4, 2024

How Potential Federal Rate Cuts Could Bring Positive Shifts to the Housing Market

August 15, 2024

August 7, 2024

Unprecedented Savings: Perfect Time to Buy!

You’ve got questions and we can’t wait to answer them.